Economics Worksheets for High School

Are you a high school student struggling to grasp the concepts of economics? Look no further, because we have a solution for you - economics worksheets! These helpful resources provide a structured and comprehensive way to practice and reinforce your understanding of various economic principles and theories. With a focus on entity and subject, these worksheets ensure that you have all the necessary tools to succeed in your economics class.

Table of Images 👆

- Home Economics Worksheets Free

- Economics Supply and Demand Worksheets High School

- Career Exploration Worksheets Middle School

- Substitute Teacher Worksheets

- Mumbai J J School of Art

- Needs and Wants Worksheet Kindergarten

- Mexico Government Worksheet

- Adult Life Skills Lesson Worksheets

- High School Photography Lesson Plans

- 11th Grade Chemistry Worksheets

- Clip Art Black and White T-Shirt

- Writing Letters Worksheets for First Grade

- Essay Writing About My First Day at School

- Three Branches of Government Tree Worksheet

- 7th Grade Social Studies Worksheets

- 7th Grade Social Studies Worksheets

- 7th Grade Social Studies Worksheets

- 7th Grade Social Studies Worksheets

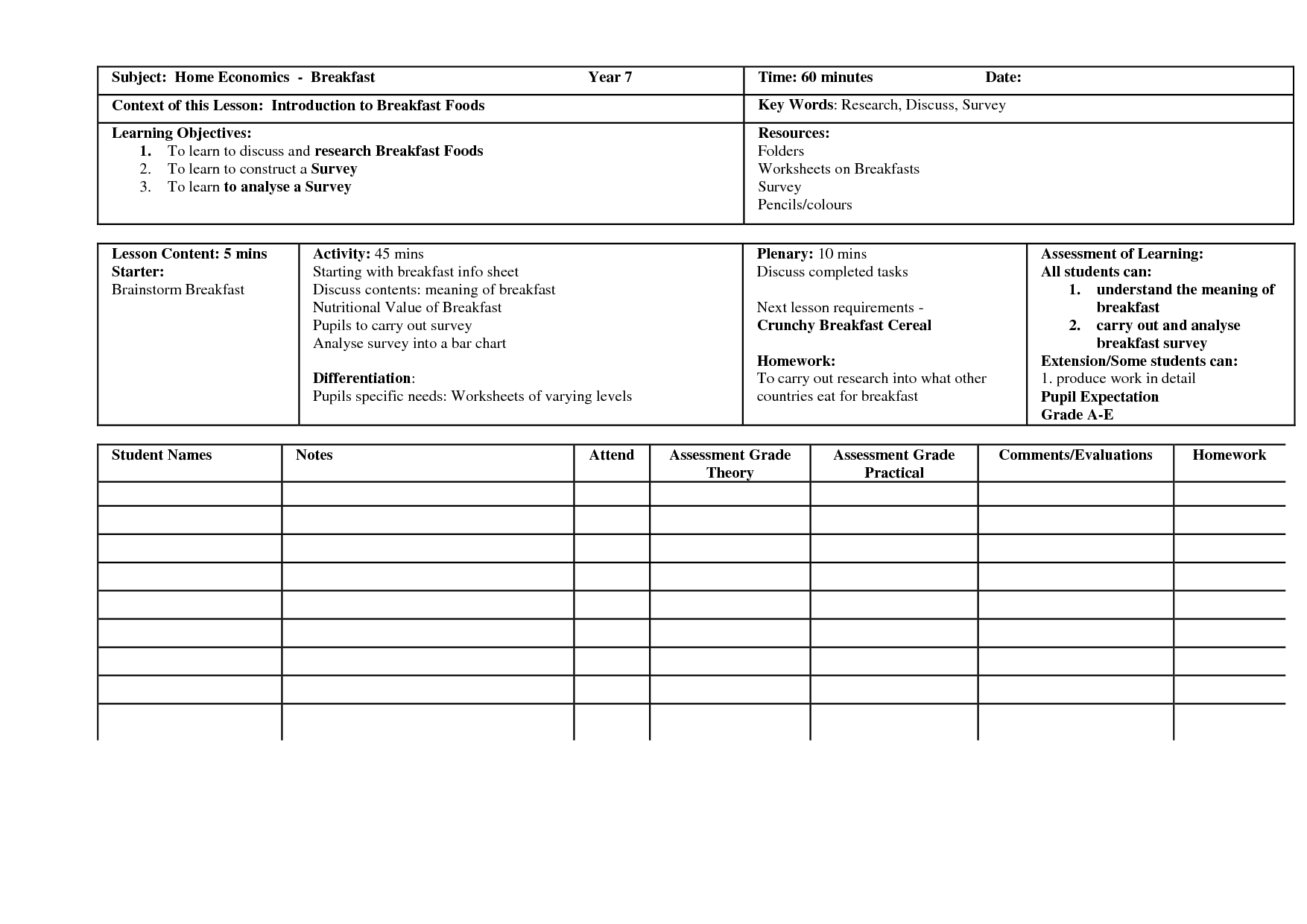

Home Economics Worksheets Free

Home Economics Worksheets Free

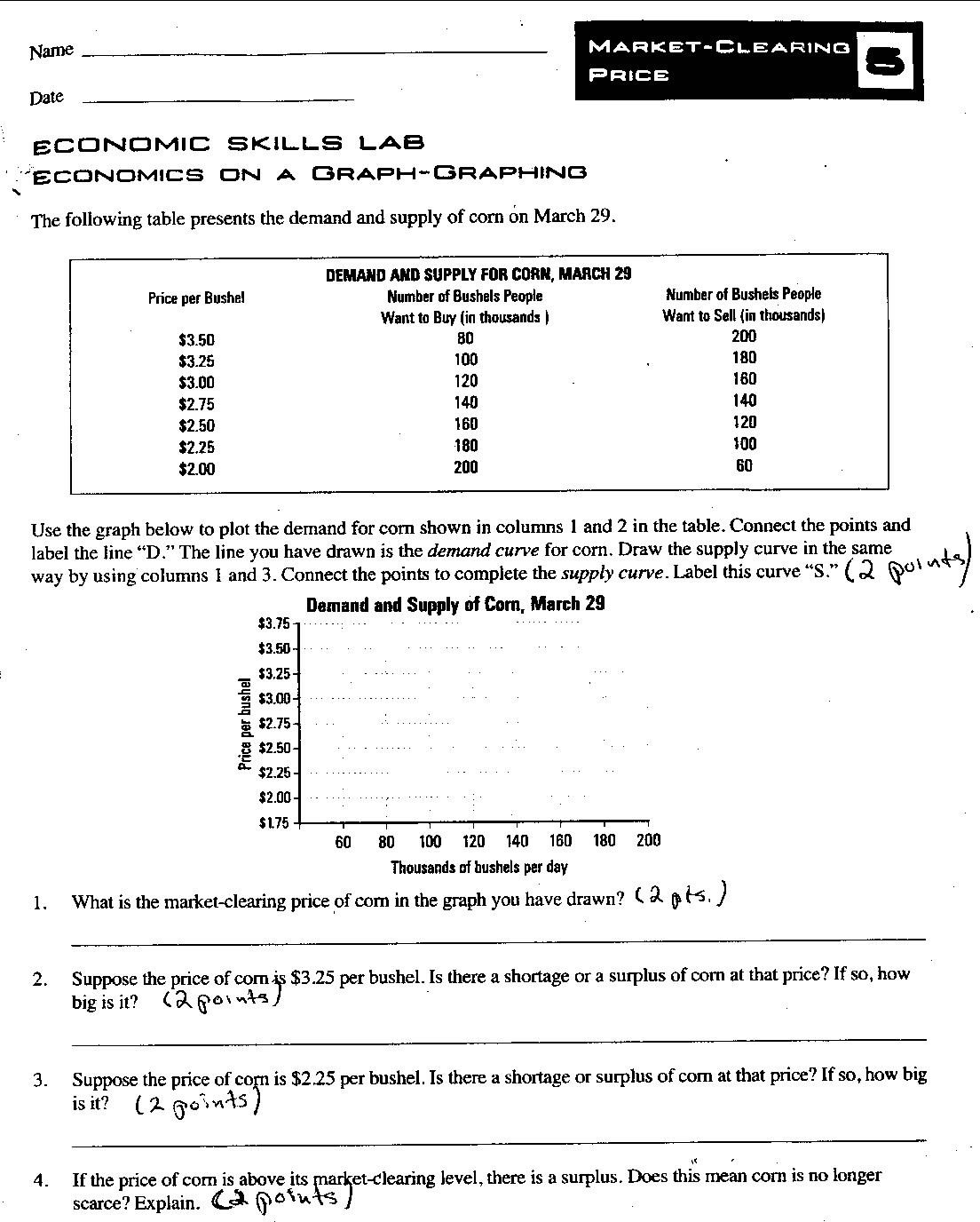

Economics Supply and Demand Worksheets High School

Economics Supply and Demand Worksheets High School

Career Exploration Worksheets Middle School

Career Exploration Worksheets Middle School

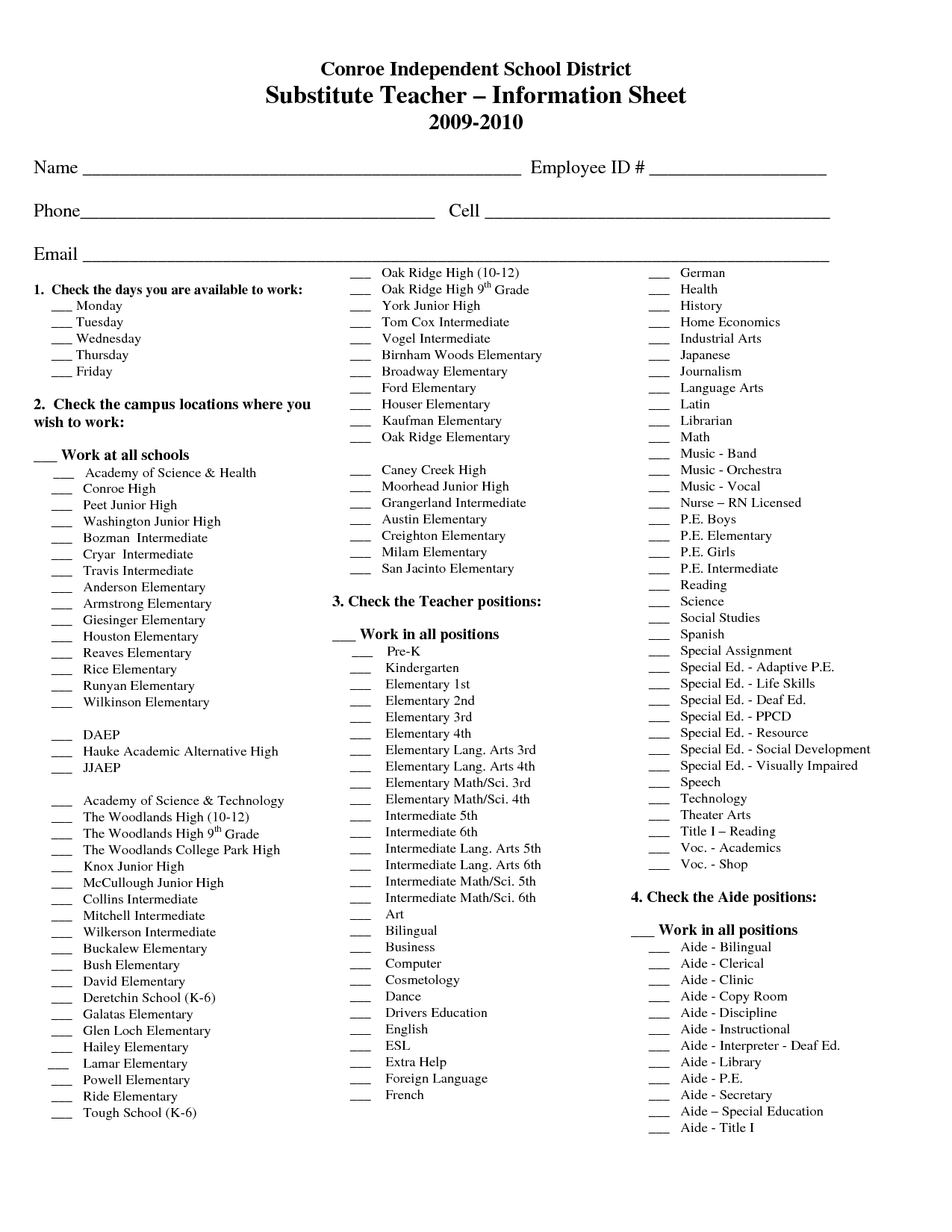

Substitute Teacher Worksheets

Substitute Teacher Worksheets

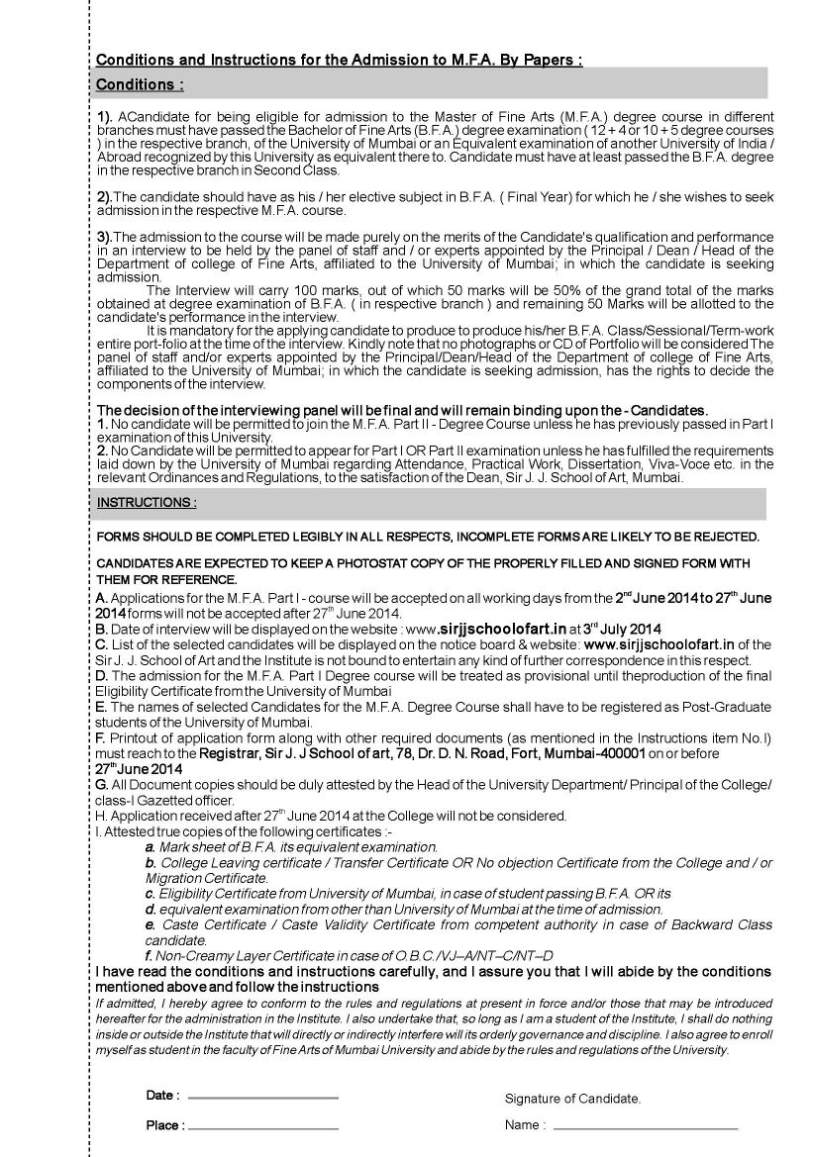

Mumbai J J School of Art

Mumbai J J School of Art

Needs and Wants Worksheet Kindergarten

Needs and Wants Worksheet Kindergarten

Mexico Government Worksheet

Mexico Government Worksheet

Adult Life Skills Lesson Worksheets

Adult Life Skills Lesson Worksheets

High School Photography Lesson Plans

High School Photography Lesson Plans

11th Grade Chemistry Worksheets

11th Grade Chemistry Worksheets

Clip Art Black and White T-Shirt

Clip Art Black and White T-Shirt

Writing Letters Worksheets for First Grade

Writing Letters Worksheets for First Grade

Essay Writing About My First Day at School

Essay Writing About My First Day at School

Three Branches of Government Tree Worksheet

Three Branches of Government Tree Worksheet

7th Grade Social Studies Worksheets

7th Grade Social Studies Worksheets

7th Grade Social Studies Worksheets

7th Grade Social Studies Worksheets

7th Grade Social Studies Worksheets

7th Grade Social Studies Worksheets

7th Grade Social Studies Worksheets

7th Grade Social Studies Worksheets

More Other Worksheets

Kindergarten Worksheet My RoomSpanish Verb Worksheets

Cooking Vocabulary Worksheet

My Shadow Worksheet

Large Printable Blank Pyramid Worksheet

Relationship Circles Worksheet

DNA Code Worksheet

Meiosis Worksheet Answer Key

Art Handouts and Worksheets

7 Elements of Art Worksheets

What is the definition of economics?

Economics is the social science that studies how individuals, businesses, governments, and societies make choices about allocating scarce resources to satisfy their unlimited wants and needs. It examines how resources are produced, distributed, and consumed in order to understand patterns of behavior and outcomes in the marketplace.

What are the three basic questions of economics?

The three basic questions of economics are: what to produce, how to produce, and for whom to produce. These questions revolve around the fundamental principles of allocating scarce resources to meet unlimited wants and needs in society.

Describe the concept of supply and demand.

Supply and demand is an economic theory that explains the relationship between the availability of a product or service (supply) and the desire for that product or service (demand). The theory states that the price of a product will increase when demand exceeds supply, and decrease when supply exceeds demand. This interaction ultimately determines the equilibrium price and quantity of goods in a market economy, impacting production, consumption, and overall market dynamics.

What is the difference between a market economy and a planned economy?

A market economy is driven by the forces of supply and demand, where prices are set by market interactions and decisions are made by individuals and businesses. In contrast, a planned economy is centrally controlled by the government, with authorities making decisions on production, distribution, and resource allocation. The key difference lies in who determines economic activities: in a market economy, it is decentralized based on market mechanisms, while in a planned economy, it is centralized and dictated by a central authority.

Explain the role of government in a market economy.

The role of government in a market economy is to create and enforce rules and regulations that ensure fair competition, protect consumer rights, and address market failures. Government intervention is needed to prevent monopolies, promote public goods, provide social safety nets, and regulate externalities. Additionally, governments oversee fiscal and monetary policies to stabilize the economy and promote long-term growth. Overall, the government's role is to balance the free market forces with the need for social welfare and economic stability.

Discuss the concept of inflation and its effects on the economy.

Inflation refers to the general increase in prices of goods and services in an economy over a period of time, resulting in a decrease in the purchasing power of a currency. Moderate inflation is considered normal and can reflect a growing economy. However, high and unpredictable inflation can have adverse effects such as reducing consumers' purchasing power, leading to a decline in real wages, increasing the cost of borrowing, distorting investment decisions, and ultimately hindering economic growth. Central banks aim to manage inflation through monetary policy tools to achieve price stability and support sustainable economic growth.

Describe the principle of opportunity cost.

The principle of opportunity cost states that the cost of any decision is not simply the financial outlay, but also includes the value of the next best alternative that was forgone as a result of choosing one option over another. In other words, by choosing a particular course of action, you are giving up the potential benefits that could have been gained from choosing a different path. This concept is fundamental in economics and decision-making, highlighting the importance of considering all possible alternatives and their associated costs before making a choice.

Explain the concept of economic efficiency.

Economic efficiency refers to a state where resources are allocated in a way that maximizes overall welfare, where no individual or entity can be made better off without making someone else worse off. This concept generally involves producing goods and services at the lowest possible cost while maximizing the value that consumers place on them. In simpler terms, economic efficiency occurs when society gets the most out of its scarce resources and every resource is allocated to its most valued use, leading to the best possible outcomes given the available resources.

Discuss the importance of entrepreneurship in a free market economy.

Entrepreneurship plays a crucial role in a free market economy by fostering innovation, creating new jobs, driving economic growth, and promoting competition. Entrepreneurs identify opportunities, take risks, and introduce new products or services that meet consumer needs. As a result, they contribute to wealth creation, increase productivity, and enhance overall economic vitality. Entrepreneurship also encourages creativity, adaptability, and resilience, which are essential qualities for navigating the rapidly changing business landscape in a free market economy. Overall, entrepreneurs are key drivers of economic progress and prosperity in a free market system.

Describe the factors that contribute to economic growth.

Some key factors that contribute to economic growth include investments in human capital and technology, improvements in infrastructure and institutions, entrepreneurship and innovation, access to financial capital, political stability, favorable government policies, and global economic trends. These factors collectively drive productivity, create new opportunities for employment and wealth generation, and stimulate overall economic development in a sustainable manner.

Have something to share?

Who is Worksheeto?

At Worksheeto, we are committed to delivering an extensive and varied portfolio of superior quality worksheets, designed to address the educational demands of students, educators, and parents.

Comments